Client Profile

| Industry | Investment of Funds and Investment in Capital Markets |

| Ownership | Locally-owned Limited Liability Partnership (LLP) registered in Malaysia |

| Status | Inactive since 2016 |

| Objective | Resolve outstanding compliance obligations for proper wind up |

Key Outcomes at a glance (engagement completed March 2026):

- 9 years of overdue SSM Annual Declarations — filed and brought current

- 11 years of unfiled LHDN tax returns (Form PT and Form E) — compiled and submitted

- SSM compounds — appealed and reduced by approximately 80%

- LHDN tax clearance letter — obtained

- LLP fully dissolved within 5 months of engagement

Background

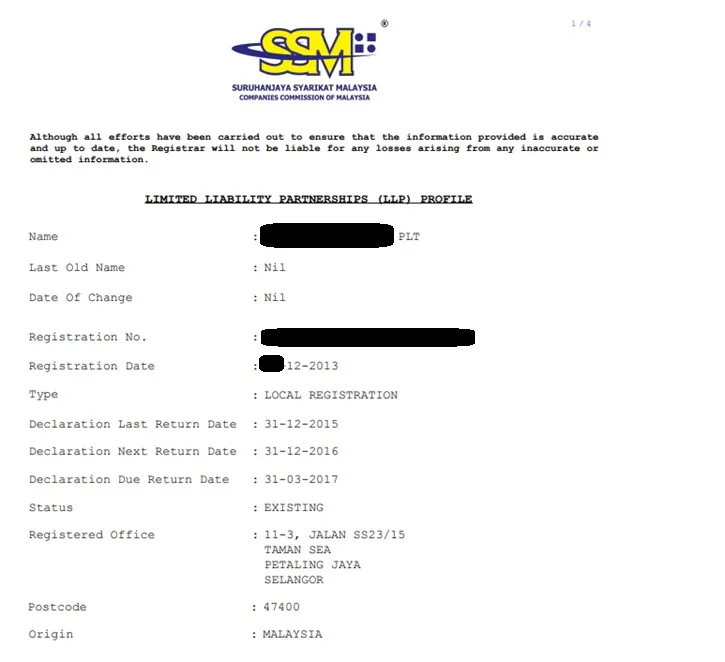

This client came to us through a referral. One of the partners reached out to ask about his LLP — a structure he and his business partner had registered back in December 2013 to undertake fund investments and capital market activities. He had also been appointed as the LLP's compliance officer at the time of registration.

The business never gained traction. The LLP went inactive around 2016, and from that point on, nothing was filed — no annual declarations to SSM, no tax returns to LHDN, no employer returns. For nearly a decade, the obligations simply accumulated.

By the time the partner contacted us, the LLP had:

- 9 years of overdue Annual Declarations with SSM under Section 68 of the Limited Liability Partnerships Act 2012

- Accumulated SSM compounds arising from the failure to lodge annual declarations under Section 68 of the LLP Act 2012 — an offence carrying fines of up to RM20,000 per instance, with a further daily default penalty of up to RM500.

- 11 years of unfiled tax returns with LHDN under Section 77A and section 83(1) of the Income Tax Act 1967. Under the Income Tax Act 1967, failure to furnish a tax return is an offence carrying fines of between RM200 and RM20,000, imprisonment of up to six months, or both — with penalties increasing for repeated offences. Persistent non-filing can also attract tax penalties of up to 300% of the tax payable.

The partners knew the LLP needed to be closed. What they didn't know was how — or whether it was even possible given the extent of the non-compliance.

The Challenge: Dormant Companies and LLPs Don't Expire on Their Own

A common misconception among business owners is that an inactive LLP or company will simply "expire" on its own. It does not. The obligations continue to accrue whether or not the business is operating, and the longer they remain unresolved, the more complex and costly the eventual clean-up becomes.

In this case, the partners had explored closure before but hit a wall. The voluntary winding-up of an LLP in Malaysia is governed by Section 50 of the LLP Act 2012, and the requirements are strict: an LLP may only apply to the Registrar for a declaration of dissolution if it has ceased to operate and has discharged all its debts and liabilities. SSM will not accept the application with outstanding compliance matters on record.

Separately, a tax clearance letter from LHDN formally confirming no objection to the dissolution is a mandatory prerequisite before the winding-up application can proceed. LHDN will not issue the clearance letter until all outstanding tax returns, including both the LLP's income tax returns (Form PT) and employer returns (Form E), have been filed and any resulting tax liabilities settled.

Both of these prerequisites demanded that the years of non-compliance be resolved first — methodically and in the correct sequence. The partners needed someone to assess the full picture, lay out exactly what was required, and then execute it from start to finish.

Our Role: Acting as Compliance Officer and Licensed Tax Agent

We stepped in as the LLP's compliance officer and tax agent in October 2025. Our first step was to conduct a full compliance assessment — mapping out every outstanding obligation across both SSM and LHDN to understand the true extent of the exposure.

We then sat down with the partners and walked them through everything: the potential exposure from the years of non-compliance, the procedures required under the Limited Liability Partnerships Act 2012 and the Income Tax Act 1967, the expected timeline, and our estimated costs. No surprises, no ambiguity — just a clear picture of what needed to happen and what it would take.

With the partners' full agreement, we commenced work in November 2025.

What we resolved:

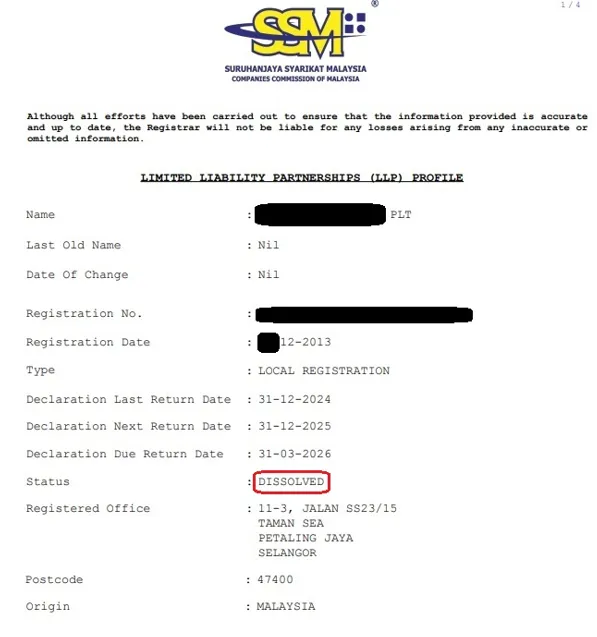

- 9 years of Annual Declarations — prepared and submitted to SSM under Section 68 of the LLP Act 2012, bringing the LLP's statutory filings fully up to date.

- SSM compounds appeal and reduction — addressed the accumulated compounds imposed for the years of non-compliance, and submitted a formal appeal to SSM requesting a reduction of the outstanding compounds. The appeal was accepted, with compounds reduced by approximately 80%.

- 11 years of income tax returns (Form PT) — compiled and filed with LHDN under Section 77A of the Income Tax Act 1967, covering every outstanding year of assessment since the LLP went inactive.

- 11 years of employer returns (Form E) — prepared and submitted to LHDN under Section 83(1) of the Income Tax Act 1967, fulfilling the LLP's employer reporting obligations for every outstanding year.

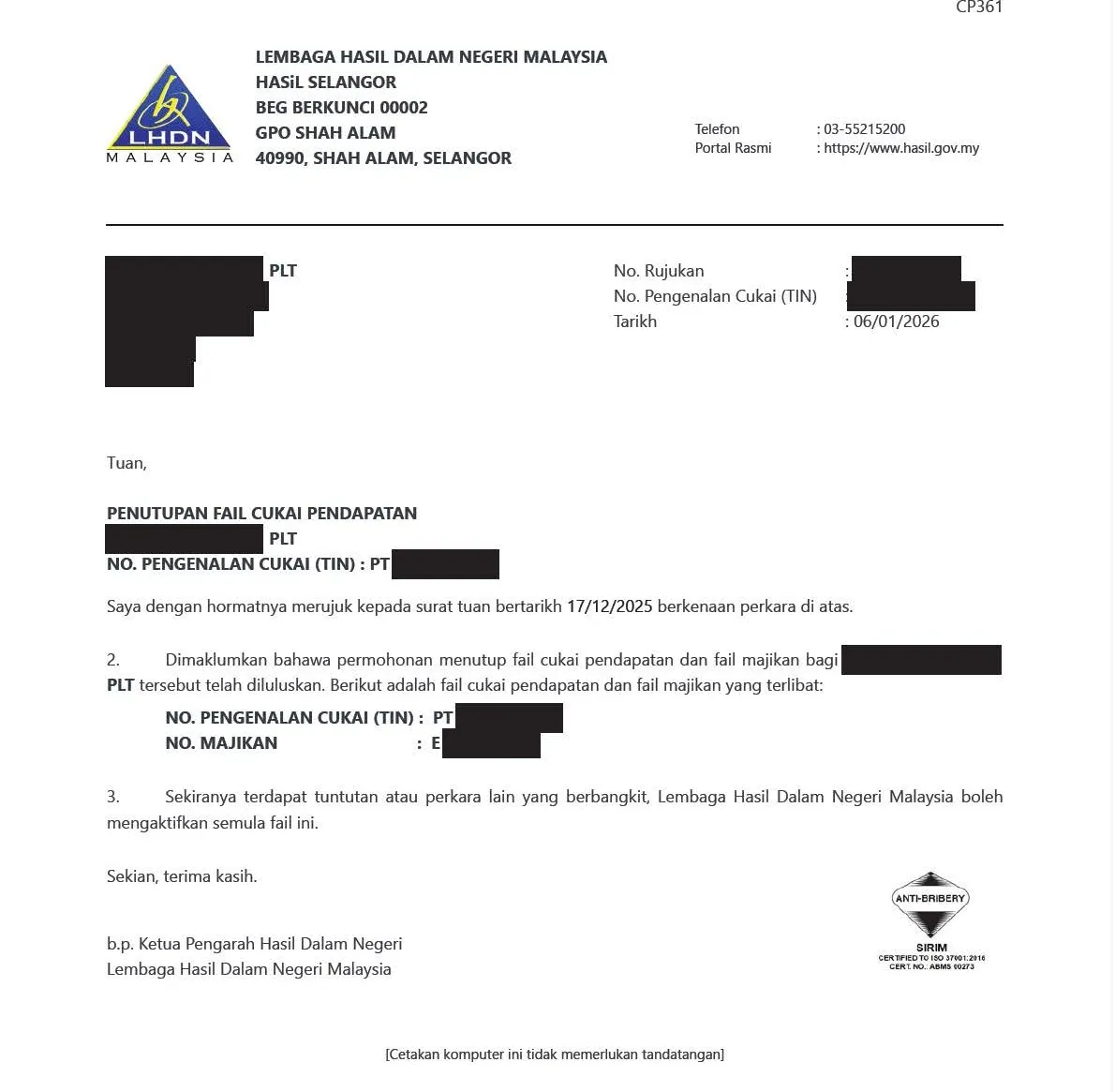

- Tax clearance letter — applied for and obtained from LHDN, confirming the LLP had no outstanding tax liabilities and no objection to the dissolution.

- Winding-up application — prepared and lodged with SSM pursuant to Section 50 of the LLP Act 2012 once all compliance prerequisites were satisfied, including newspaper advertisements in Bahasa Malaysia and English, statutory declaration attested by a Commissioner for Oaths, and registered notices to all partners.

- Closure of the LLP — completed upon full distribution of surplus assets to the partners.

Closure of the LLP's tax file — upon completion of the winding-up, we applied to LHDN for the formal closure of the LLP's income tax and employer files. LHDN approved the closure, confirming that all tax obligations had been fully discharged.

The entire process from commencement in November 2025 to the LLP being fully wound up was completed within five months, by March 2026.

The Result: A Decade of Non-Compliance Resolved in Five Months

A decade of accumulated non-compliance, untangled and closed out in five months.

What had been a source of lingering uncertainty for nearly ten years was resolved in an orderly manner. The partners walked away with a properly wound-up LLP, no outstanding obligations with SSM or LHDN, and — perhaps most importantly — no further exposure from a dormant entity they had long stopped thinking about.

Why This Matters

Not every engagement is about growth. Sometimes the right outcome is a clean and responsible exit — and that requires the same level of rigour and attention as setting up a business in the first place.

For anyone reading this with a dormant company or LLP in Malaysia that has been sitting idle with years of unfiled returns, the compliance obligations don't disappear. Annual declarations to SSM, income tax returns and employer returns to LHDN continue to accrue whether or not the business is operating.

SSM compounds for late filings can reach up to RM20,000 per offence, with additional daily default penalties of RM500. On the tax side, LHDN penalties for unfiled returns can range from RM200 to RM20,000 per year of assessment — and the professional fees required to untangle years of accumulated non-compliance will inevitably be higher than the cost of resolving matters promptly. The longer a dormant entity is left unattended, the more expensive and complex the eventual clean-up becomes.

The good news is that with the right guidance, it can be resolved — methodically, transparently, and without unnecessary stress. As this case demonstrates, even a decade of non-compliance can be untangled and closed out in a matter of months.

We take the same approach regardless of whether a client is incorporating a new company, raising capital, or winding down. Clear steps, full visibility on what to expect, and consistent follow-through until the matter is closed.

Need to Wind Up a Dormant Company or LLP?

If you have a dormant company or LLP with outstanding compliance matters, contact us for an assessment. We will give you an honest picture of where things stand and what it will take to resolve them.