Regulatory compliance can be both time-consuming and costly for businesses, especially small and medium-sized enterprises (SMEs). To alleviate these burdens, the Companies Commission of Malaysia (SSM) has revised the audit exemption framework under Practice Directive 10/2024, effective 1 January 2025. This update significantly expands eligibility, allowing more private companies to benefit from reduced compliance costs while ensuring financial accountability.

For businesses considering audit exemption, it is crucial to understand the new eligibility criteria, compliance requirements, and the steps needed to make an informed decision.

1. Evolution of the Audit Exemption Framework

Malaysia introduced audit exemption on 4 August 2017 under Practice Directive 3/2017, primarily to support micro and small enterprises in reducing regulatory costs. However, recognizing the need for broader accessibility, SSM revised the framework with higher thresholds under the Practice Directive 10/2024, issued on 16 December 2024.

It’s important to note that the new Audit Exemption Framework introduced under Practice Directive 10/2024 is applicable for financial statements with annual period commencing on or after 1 January 2025. It means that if your company is having 31st December as the year-end, your first set eligible for audit exemption under the new guideline will be the financial statements for the financial year ended 2025, which commence from 1 January 2025 to 31 December 2025.

This revision aligns Malaysia’s corporate compliance policies with international standards while addressing concerns raised by business stakeholders regarding the previous limitations of the exemption criteria.

For the latest SSM Audit Exemption Guidelines, refer to: 🔗 SSM Official Audit Exemption Portal

2. New Qualifying Criteria

A private company qualifies for audit exemption under the new guideline (PD10/2024) if it meets at least two (2) of the following criteria for both the current and immediate past financial years:

(Note: Under the previous guideline (PD3/2017), the company was required to meet all three (3) criteria to qualify for the exemption.)

| Criteria | Under previous guideline (PD3/2017) | Under new guideline (PD10/2024) |

| Annual revenue | ≤ RM100,000 | ≤ RM3,000,000 |

| Total assets | ≤ RM300,000 | ≤ RM3,000,000 |

| No. of employees | ≤ 5 employees | ≤ 30 employees |

| Applicable to | Financial statements commencing on or before 31 December 2024(1) | Financial statements with annual period commencing on or after 1 January 2025(1) |

(1) If your company has a financial year ending on 31 December, Practice Directive 3/2017 will apply to financial statements for the year ending 31 December 2024. The new guideline, Practice Directive 10/2024, will take effect for financial statements for the financial year ending 31 December 2025, covering the period from 1 January 2025 to 31 December 2025. However, the threshold criteria will be implemented gradually, as outlined below.

Additionally, dormant companies (those inactive since incorporation or during the immediate past and current financial year) are also eligible for exemption.

Phased Implementation

To ensure a smooth transition, the threshold criteria will be implemented gradually over three years:

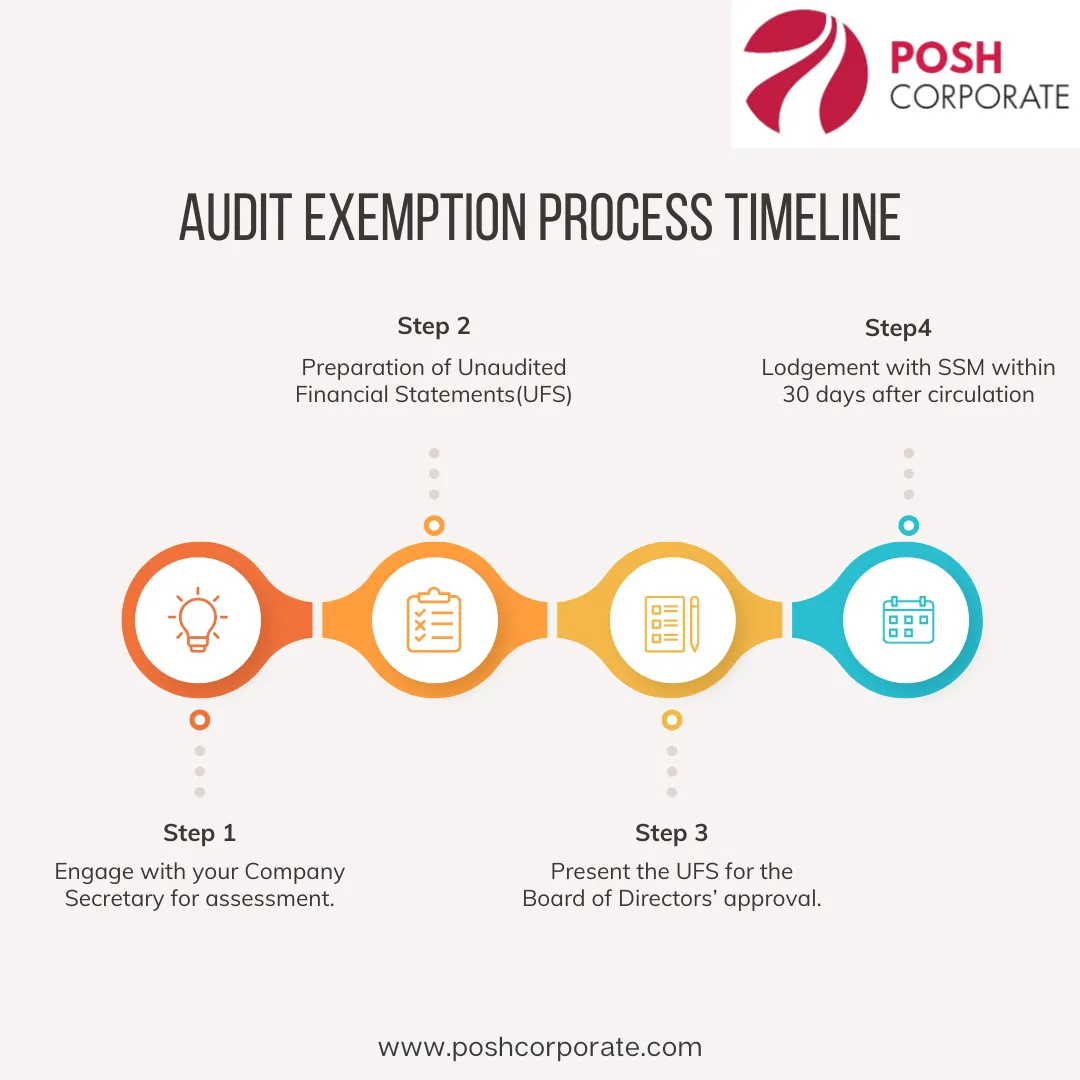

3. What the Company need to do?

Reference: SSM’s Official Guide refer to: PD10-2024: Qualifying Criteria for Audit Exemption

4. Our insights to this Unaudited FS

While audit exemption provides a pathway to reduced compliance costs, companies must carefully assess the long-term impact on their financial transparency, reputation, and stakeholder relationships. Opting for audit exemption should align with your business’s growth trajectory, financing needs, and regulatory obligations.

Key Considerations Before Opting for Audit Exemption

-

Compliance with MPERS & Regulatory Standards – Unaudited financial statements must adhere to the Malaysian Private Entities Reporting Standards (MPERS) and provide a true and fair view of the company’s financial position.

-

Stakeholder Expectations & Financial Credibility – Banks, investors, and regulatory bodies may still require audited financials for loan applications, funding, or contractual agreements. If external financing is a priority, maintaining an audit trail can enhance credibility.

-

Regulatory & Industry-Specific Requirements – Certain businesses, particularly those with bank loans, government grants, or investor obligations, may need to continue auditing their financials despite exemption eligibility. Always verify with stakeholders before making a final decision.

-

Maintaining Transparency & Business Integrity – While exemption simplifies compliance, accurate record-keeping and financial transparency remain crucial for corporate governance and operational efficiency.

For further insights, refer to: The Edge Malaysia’s analysis on audit exemption

Advisory Insights

As your trusted advisor, we recommend a strategic evaluation before electing for audit exemption. The decision should consider:

-

Your Company’s Long-Term Goals – Will audit exemption support or hinder your expansion plans?

-

Stakeholder Confidence – How will it impact relationships with investors, lenders, and regulatory bodies?

-

Operational & Financial Efficiency – Does exemption allow your business to reallocate resources effectively while maintaining financial integrity?

Our team of tax agents, company secretaries, and business advisors is here to provide tailored guidance, ensuring your business leverages audit exemption effectively while maintaining compliance and stakeholder trust.

By making an informed decision, businesses can maximize the benefits of audit exemption while safeguarding their financial credibility and long-term sustainability.

5. FAQs

1. Can a company with corporate shareholders qualify for audit exemption?

Yes, as long as the company meets the qualifying criteria, the presence of corporate shareholders does not disqualify it from audit exemption.

2. Does opting for audit exemption remove the obligation to file financial statements?

No, companies must still prepare and circulate unaudited financial statements and submit them to SSM within 30 days.

3. Do companies need to apply for audit exemption?

No formal application is required. Companies automatically qualify if they meet the eligibility criteria. Companies are encouraged to engage professional company secretaries and accountants for assessment.

4. How does audit exemption affect income tax obligations?

Audit exemption does not remove the obligation to comply with tax regulations. Companies must still file tax returns and provide financial statements upon request by LHDN (Inland Revenue Board of Malaysia). Please find the LHDN Income Tax Guide

5. How should companies determine their number of employees for eligibility?

The number of employees is based on the number of full-time employees employed by the company at the end of each relevant financial years. For the purpose of PD10/2024, full-time employees means paid workers working for not less than six (6) hours a day for at least 20 days a month or working for at least 120 hours a month.

Full-time workers include local, foreign, contract workers and workers undergoing probationary period but excluding:

-

family members or friends who are unpaid or receiving irregular wages while working in the company.

-

a director who is also working as a full-time employee;

-

a shareholder who is also working as a full-time employee; or

Conclusion

Audit exemption presents a relief option for Malaysian private companies to reduce compliance costs while maintaining regulatory transparency. However, businesses must carefully assess their financial reporting obligations and long-term objectives before opting for exemption.

For professional guidance on compliance, financial reporting, and tax obligations, I strongly recommend consulting a qualified Company Secretary, Tax Consultant, or Business Advisor to ensure a smooth and compliant transition. For more information, visit SSM Official Audit Exemption information page